French Fire Fighting Aircraft and the Soaring Global Market: A Shocknaue Entertainment News Insight

The global market for firefighting aircraft, essential tools in combating widespread blazes, is witnessing significant growth. Valued at $9.5 billion in 2024, this crucial sector is projected to dramatically increase to $27.2 billion by 2040, demonstrating a Compound Annual Growth Rate (CAGR) of 6.9% from 2025 to 2040. This expansion highlights the escalating global need for advanced aerial firefighting capabilities, including specialized French Fire Fighting Aircraft acquired by nations like France to bolster their emergency response fleets.

Market Overview and Definition

A firefighting aircraft is a specially designed or modified aviation asset deployed for aerial firefighting operations, primarily against wildfires and other extensive conflagrations. These aircraft are vital in wildfire suppression efforts, delivering crucial payloads like water, fire retardants, or foam to affected regions, particularly those that are remote or difficult to access from the ground. The category encompasses various types, including fixed-wing air tankers, scooper aircraft, and multi-mission planes, as well as rotary-wing helicopters outfitted with equipment like Bambi Buckets or internal tanks. Deployed by government bodies, private entities, and military forces worldwide, these aircraft boast varying capabilities. For instance, large air tankers can dispense thousands of gallons of retardant, while smaller helicopters offer precision drops. Recent technological advancements, such as satellite tracking, AI-powered fire detection systems, and modern dispersal methods, have substantially improved the efficiency of aerial firefighting operations. As the frequency and intensity of wildfires continue to rise globally, many nations are actively expanding and modernizing their aerial firefighting fleets, integrating newer technologies, and enhancing international cooperation to improve overall wildfire management and disaster preparedness strategies.

Market Dynamics: Drivers and Restraints

The increasing frequency and intensity of wildfires across the globe are the primary forces driving the demand for firefighting aircraft. Traditional ground-based firefighting methods often prove insufficient for containing large-scale wildfires, especially in remote or hard-to-reach terrains. Aircraft offer a critical advantage by swiftly reaching fire zones, delivering substantial volumes of suppressants, and more effectively halting fire spread. Governments and firefighting agencies are actively expanding their aerial fleets to improve response capabilities, leading to increased procurement and modernization projects.

For example, a significant development highlighting this trend and the importance of capable assets like French Fire Fighting Aircraft (or aircraft procured by France) occurred in March 2025. The Canadian Commercial Corporation (CCC) finalized a government-to-government (G2G) contract with France’s Directorate General of Armaments (DGA), under the French Ministry of Armed Forces, for the acquisition of two De Havilland Canadair 515 aircraft. This purchase directly strengthens France’s aerial firefighting fleet, significantly enhancing its capacity to combat escalating wildfire threats. The Canadair 515, renowned for its substantial water-carrying capacity and rapid deployment capabilities, will improve France’s fire suppression efforts, ensuring greater efficiency in fighting wildfires. Additionally, technological advancements in firefighting aircraft, including enhanced tank capacity, autonomous operational potential, and improved maneuverability, are further fueling market demand. Public-private partnerships and international collaborations also contribute significantly to fleet expansion efforts. With climate change exacerbating wildfire risks, investments in aerial firefighting solutions are expected to grow, reinforcing the demand for these essential aircraft across various regions.

The surge in fire-related incidents within the oil and gas industry has also markedly increased the demand for firefighting aircraft. Facilities such as oil refineries, offshore drilling platforms, and storage sites are highly susceptible to fires that can spread rapidly due to the presence of flammable materials. In such hazardous environments, traditional firefighting methods can be inadequate, making aerial firefighting aircraft crucial for prompt response and containing large-scale industrial fires. Fixed-wing and rotary-wing aircraft equipped with advanced fire retardant and water-dropping systems play a vital role in minimizing damage and preventing catastrophic losses. Both governments and private sector entities are increasingly investing in specialized firefighting aircraft to enhance their emergency response capabilities in high-risk industrial zones. Furthermore, the integration of unmanned aerial vehicles (UAVs) for monitoring and assessing fire hazards in oil and gas infrastructure is also contributing to market growth by improving safety measures and operational resilience in the industry. Some might compare the scale of these modern aviation assets to historical needs, pondering developments like ww2 japanese fighter aircraft or considering the current state of china jet fighter aircraft in a different context.

However, the market faces restraints, notably delayed deliveries of aircraft. These delays significantly impact the availability of firefighting aircraft globally, hindering wildfire response efforts. Procurement delays often stem from supply chain disruptions, manufacturing challenges, and bottlenecks in regulatory approvals, causing setbacks in fleet expansion and modernization plans. As a consequence, governments and firefighting agencies encounter operational gaps, limiting their ability to respond effectively to the rising number of wildfire incidents. While demand for high-capacity, advanced firefighting aircraft grows, delivery delays result in extended lead times, higher costs, and restricted access to essential aerial firefighting resources. These factors negatively affect disaster preparedness, compelling agencies to either rely on older fleets or temporary leasing arrangements, which may not offer optimal effectiveness. Moreover, protracted delays can discourage potential buyers from investing in new firefighting aircraft, thereby slowing market growth. Addressing these challenges through streamlined production processes, accelerated approval procedures, and bolstering supply chain resilience is essential to ensure the timely availability of aircraft and improve global wildfire response capabilities. The challenges faced in acquiring these specialized aircraft are a stark contrast to the capabilities seen in domains like the best fighter aircraft in the world today, which highlights the distinct needs of different aviation sectors.

Segment Analysis

The firefighting aircraft market is segmented by aircraft type, tank capacity, maximum takeoff weight, range, and region, providing a detailed look at its composition.

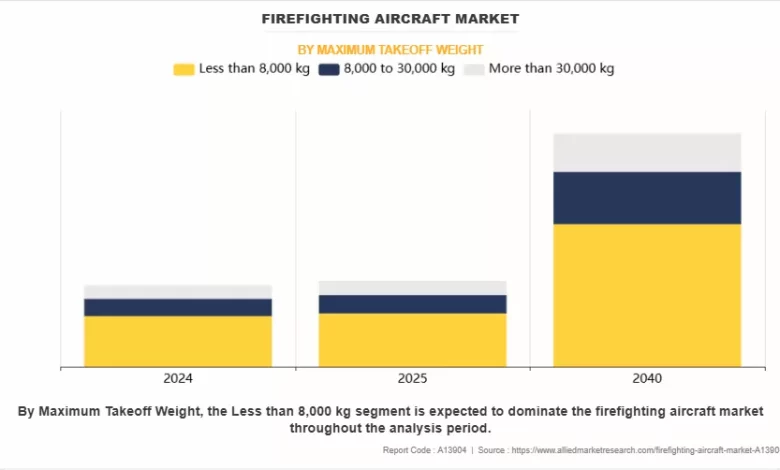

Based on maximum takeoff weight, the market is categorized into less than 8,000 KG, 8,000 to 30,000 KG, and more than 30,000 KG. The segment of aircraft weighing less than 8,000 KG generated the largest revenue in 2024. This reflects a significant use of smaller, potentially more maneuverable aircraft or helicopters in various firefighting scenarios. The overall increase in the use of aircraft for wildfire suppression globally is a key factor driving demand across all weight categories, as rapid response and containment become ever more critical in the face of worsening wildfires linked to climate change. Market share of firefighting aircraft by maximum takeoff weight, highlighting the less than 8,000 KG category leading in 2024.

Market share of firefighting aircraft by maximum takeoff weight, highlighting the less than 8,000 KG category leading in 2024.

By aircraft type, the market includes fixed-wing planes (airplanes) and rotary-wing aircraft (helicopters). In 2024, fixed-wing aircraft held the largest market share. This segment includes large air tankers and scooper aircraft capable of delivering massive amounts of suppressants over wide areas. Governments and private operators are investing heavily in expanding and modernizing their fleets, including fixed-wing assets like the Canadair 515 sought by France, to enhance firefighting capabilities, boost operational efficiency, and ensure faster disaster response. This investment further fuels demand within the firefighting aircraft industry. Considering the specialized nature of these planes, it’s interesting to note the historical trajectory of aviation, perhaps comparing them to the specialized designs of japanese ww2 fighter aircraft or pondering the engineering feats behind the fastest fighter aircraft in the world. Segmentation of the firefighting aircraft market by aircraft type, showing fixed-wing aircraft having the largest share in 2024.

Segmentation of the firefighting aircraft market by aircraft type, showing fixed-wing aircraft having the largest share in 2024.

Regarding tank capacity, the market is divided into less than 10,000 liters, 10,000 to 30,000 liters, and more than 30,000 liters. The demand across these segments is driven by the factors mentioned earlier: the increase in fire-related incidents within the oil and gas industry and the rising frequency of wildfires. These events necessitate aircraft capable of carrying substantial suppressant volumes. However, as noted, the market’s growth is somewhat tempered by delays in the delivery of new firefighting aircraft, hindering the timely deployment of these much-needed assets. Breakdown of the firefighting aircraft market by tank capacity, indicating growth driven by increasing fire incidents.

Breakdown of the firefighting aircraft market by tank capacity, indicating growth driven by increasing fire incidents.

Range segmentation categorizes aircraft by their operational radius: less than 1,000 KM, 1,000 to 3,000 KM, and more than 3,000 KM. The report highlights that a surge in long-term contracts and agreements presents a lucrative opportunity for the firefighting aircraft market. These agreements ensure stable revenue streams and sustained business growth, as governments and private operators increasingly seek multi-year commitments for reliable aerial firefighting support, particularly as wildfire risks escalate globally. This indicates a growing need for aircraft capable of sustained operations or reaching distant fire zones, suggesting importance across the range segments. The firefighting aircraft market segmented by range, illustrating opportunities driven by long-term contracts.

The firefighting aircraft market segmented by range, illustrating opportunities driven by long-term contracts.

Geographically, the market is analyzed across North America, Europe, Asia-Pacific, and LAMEA (Latin America, Middle East, and Africa). North America is projected to be the most lucrative region during the forecast period from 2025 to 2034. This is likely due to the scale and frequency of wildfires in the region and significant investment capacity. Strategic partnerships between aircraft manufacturers, firefighting agencies, and leasing companies in regions like North America facilitate access to modernized fleets, thereby improving operational efficiency. Long-term agreements also strengthen international cooperation, fostering advancements in aerial firefighting capabilities and disaster management strategies worldwide. This regional analysis underscores where the demand for aircraft, potentially including capabilities similar to those sought by the french fire fighting aircraft fleet expansion, is strongest. Regional analysis of the firefighting aircraft market, identifying North America as the most lucrative segment.

Regional analysis of the firefighting aircraft market, identifying North America as the most lucrative segment.

Competitive Landscape and Key Developments

The global firefighting aircraft market is characterized by a notable presence of established vendors, leading to a competitive environment. Key players profiled in the market report include SAAB, ShinMaywa Industries, Ltd., COULSON GROUP, Conair Aerial Firefighting, Lockheed Martin Corporation, Kaman Corporation, AIRBUS, Textron, Inc., Leonardo S.p.A., and De Havilland Aircraft of Canada Limited. Companies possessing extensive technical expertise and financial resources are expected to gain a competitive edge by meeting market demands, which currently often outstrip supply due to challenges like delivery delays. The competitive intensity is anticipated to increase further with ongoing technological innovations, product line expansions, and various strategic initiatives adopted by these key vendors.

Recent strategic moves by major players highlight the focus on enhancing capabilities and securing market position. In January 2025, Conair acquired the Daher TBM 960 aircraft, a move aimed at strengthening its wildfire suppression capabilities. The TBM 960’s speed, efficiency, and advanced avionics are seen as valuable assets for rapid aerial firefighting operations, allowing quicker access to fire zones and improved support for ground teams, thereby enhancing overall wildfire containment and mitigation efforts. Another significant development occurred in November 2023 when Saab signed a new contract with the Swedish Civil Contingencies Agency (MSB). This agreement ensures the continued provision of aerial firefighting aircraft, along with necessary crew and logistical support, securing a robust firefighting capability and enabling swift response to wildfires through well-equipped aircraft and experienced personnel. These developments illustrate the ongoing efforts by manufacturers and service providers to meet the increasing global demand.

Top Impacting Factors and Historical Data

The global firefighting aircraft market is poised for significant growth, driven by several key factors. These include a rising need for new generation engines and transmission units to enhance aircraft performance and efficiency, the growing adoption of lightweight aircraft components to improve payload capacity and maneuverability, and increasing military expenditure and spending that often includes aerial assets applicable to firefighting. Additionally, the increasing integration of advanced airframe technologies specifically for firefighting aircraft and a surge in the overall aircraft fleet alongside technological advancements are expected to create lucrative opportunities for market expansion during the forecast period. However, the market’s potential is somewhat limited by technical issues occasionally associated with these complex aircraft and stringent regulations governing aircraft components and operations, which can impact production and deployment.

Historically, the global firefighting aircraft market has been competitive, shaped by the strong presence of existing vendors. Companies with substantial resources have traditionally held an advantage. The market’s competitive landscape is expected to intensify, fueled by ongoing technological advancements, the introduction of new products and variants, and diverse strategies pursued by the leading vendors to capture market share and meet the evolving demands for aerial firefighting solutions.

Report Highlights Overview

Summarizing key findings from the market report, the global firefighting aircraft market is projected to reach $27.2 billion by 2040, growing at a CAGR of 6.9%. The forecast period covers 2024 to 2040. The report spans 391 pages and includes segmentation analysis by Maximum Takeoff Weight (Less than 8,000 kg, 8,000 to 30,000 kg, More than 30,000 kg), Aircraft Type (Fixed Wing or Airplanes, Rotorcraft or Helicopters), Tank Capacity (Less than 10,000 litres, 10,000 to 30,000 litres, More than 30,000 litres), and Range (Less than 1,000 km, 1,000 to 3,000 km, More than 3,000 km). Geographically, the market is analyzed across North America (U.S., Canada, Mexico), Europe (UK, Germany, France, Russia, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, Australia, Thailand, Malaysia, Indonesia, Rest of Asia-Pacific), and LAMEA (Brazil, South Africa, Saudi Arabia, UAE, Argentina, Rest of LAMEA). Key market players include major names like COULSON GROUP, Lockheed Martin Corporation, Leonardo S.p.A., Kaman Corporation, ShinMaywa Industries, Ltd., Textron, Inc., De Havilland Aircraft of Canada Limited, SAAB, Conair Aerial Firefighting, and AIRBUS.

Conclusion

The firefighting aircraft market is on a robust growth trajectory, driven by the undeniable increase in global wildfire incidents and the growing need for effective, rapid response capabilities. The market’s expansion, highlighted by projected multi-billion dollar values, underscores the critical role of aerial assets in modern disaster management. While challenges like delivery delays exist, ongoing technological advancements and strategic investments, such as the significant acquisition of Canadair 515 aircraft aimed at bolstering the french fire fighting aircraft fleet, signal a strong commitment to enhancing aerial firefighting capabilities worldwide. This dynamic sector continues to evolve, adapting to the increasing demands imposed by climate change and industrial risks, and remains a vital area for global safety and environmental protection.